Singapore, 17 Mar 2017 – In an unexpected move on 10th March, the government announced some changes to the set of property cooling measures which were progressively introduced from 20th February 2010 to 9th December 2013.

There were four main parts to the announcement.

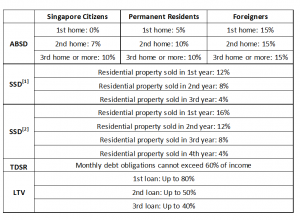

First, the Additional Buyer’s Stamp Duty (ABSD) and Loan to Value (LTV) limits are to remain unchanged. Singaporean buyers will need to pay ABSD if they purchase a second residential property and more while Permanent Residents and foreigners will incur ABSD from their first home purchase. The LTV ratio remains at a maximum of 80 per cent for private residential property loans.

Second, the Seller’s Stamp Duty (SSD) would be modified for buyers who purchase residential properties on or after 11th March 2017. Previously, the SSD was payable if homeowners sell off their properties within four years of purchase, at a rate of between four to 16 per cent. The new SSD has had its holding period revised downwards to three years and the duty rate has been reduced by four percentage points for every year. The new SSD rates now range from four per cent for residential properties sold in the third year to 12 per cent for those sold in the first year.

Third, the Total Debt Servicing Ratio (TDSR) was relaxed so as to allow for borrowers to monetise their properties. The Monetary Authority of Singapore will no longer apply the TDSR framework to mortgage equity loans with LTV ratios of 50 per cent and below.

Last, a new stamp duty treatment for the acquisition and disposal of equity interest in property holding entities has been introduced. Transactions involving residential properties will be subject to the same stamp duty rates regardless of whether through a direct sale of the property or through the sale of shares in the holding entity.

To the typical property buyer and investor, the tweak to the SSD is the only material one. As there is hardly any speculation in the residential property market, the tweaking of the SSD holding period and rates is a very safe and calibrated approach. It brings relief and a way out for investors and property owners who may have to dispose of the property bought in the short term without the additional burden of SSD (if sold in the 4th year), or having to pay a reduced SSD should they have to sell within the 3 year holding period. The additional flexibility in the timing of sale will certainly benefit both owner occupiers and investors.

Though there is much to cheer about, this change in SSD period and rates is only applicable to residential properties bought on and after 11 March 2017. There is no change to SSD holding period and rates for residential properties bought between 14 January 2011 and 10 March 2017.

As such, this measure is a forward looking one that allows prospective residential property purchasers to re-calibrate their calculations, expectations and holding period, should they purchase residential properties on or after 11 March 2017. While it may change slightly how investors and home-buyers look at the timeline on holding the properties, it is not expected that this tweak will have the effect of pushing up property prices in both the primary and secondary market.

In today’s market, opportunities are plentiful for home buyers. The main dampers of buying demand, the ABSD and TDSR, are still in force. Hence, developers and individual sellers will still have to price their properties realistically in order to achieve the desired sales numbers within the marketing period.

Already, before the tweak to the SSD, figures from the Urban Redevelopment Authority already show that developer sales are picking up, with 977 private residential units sold in February 2017. This figure is 2.6 times that of January. March’s sales figures are expected to be even higher.

With the new SSD in place, investors will probably favour newly launched projects, as the three year holding period coincides with the approximate construction time of the development. This allows investors the flexibility to sell off their unit upon completion of the project without incurring any levy. Also, given the weak rental market currently, buying an uncompleted project allows investors to wait out the downturn.

In addition, developers have deliberately kept the overall quantum of each unit affordable so as to remain attractive. With ample supply in the market, these investors have many choices.

Developers have just started launching their 2017 projects. The Clement Canopy, Grandeur Park Residences and Park Place Residences At PLQ have all met with positive response from investors.

For a “safer” bet, investors could look at developments which are near commercial clusters or have easy access to public transportation. These projects will generally see higher demand for housing units due to a ready tenant pool, and are usually more resilient to market shocks.

For owner occupiers, good deals are still to be found in the resale market. For instance, in February, some mass market properties were sold at an approximate 20 per cent discount to their purchase price a few years back. For the wealthy, now might be a good time to enter the luxury market. Prices have only decreased by 1.2 per cent over 2016, compared to the three per cent decrease for the overall market. In addition, there have been several cases where buyers picked up very good bargains. For example, a unit in Orchard Scotts was purchased for $3.68 million, less than half the $8.5 million the previous buyer paid for it. At Seascape, a development in Sentosa Cove, a unit was transacted for $6.2 million, while the owner paid $12.8 million for the same property in 2010.

While this time around, the tweaking of the cooling measures is a minor one, we look to the intent rather than form. It would perhaps be an indication that the government is finally prepared to loosen some of the policies now that the property market is on firmer footing. Buyers might be tempted to postpone their plans to wait for more measures to be tweaked. However, as more measures are eased, prices will start to rise. Hence, instead of trying to time their purchase, buyers would be better off buying when they need to, at a reasonable price.

Summary table of current property measures

Source: Inland Revenue Authority of Singapore, Monetary Authority of Singapore, ERA Research

[1] If property is bought on or after 11 March 2017

[2] If property is bought between 14 January 2011 and 10 March 2017

By Eugene Lim, Key Executive Officer and Seah Yao Hui, Assistant Manager, Research